Q2-2022 Dynamk Life Science Industrials INSIGHTS: Trends, Transactions & Headlines

In This Report

M&A Events

Top Headlines

Dynamk Insights

VC Investments

Recommended Reads

We have seen a dramatic slow down in Q2 2022 with deal count down to low double digits and a near complete freeze of M&A activity - 4 recorded transactions with undisclosed transaction amounts. The IPO window was virtually shut in Q2 as VC-backed public listings reached a 13-year quarterly low (source: Pitchbook). We’ve also seen revenue multiples come down from the overly frothy levels down to more reasonable levels.

Top Headlines

Recursion & Roche, Genentech deal could mean +$1B in ongoing projects for AI drug discovery

In this wide-ranging collaboration, AI-powered drug designer Recursion secures $150M upfront for the use of their molecule mining technology with over 40 individual ongoing projects in total.

Full Article

Resilience Announces $625 Million Series D Financing

The $625 is in addition to a $600M series C round in August 2021. The funds will be used to invest in its infrastructure through strategic collaborations, acquisitions, organic growth, and international expansion.

Full Article

Regenerative medicine sees $22.7B in investments in 2021

A recent article highlighted 2021 achievements in the Regen Med market segment including six new cell, gene, and tissue-based therapies approved and record raise in investments. Gene therapy and cell-based companies saw $10.2 billion and $10.1 billion, respectively. Cell therapy followed with $2 billion and tissue engineering biotechs garnered $341 million.

Full Article

Dynamk Capital Insights

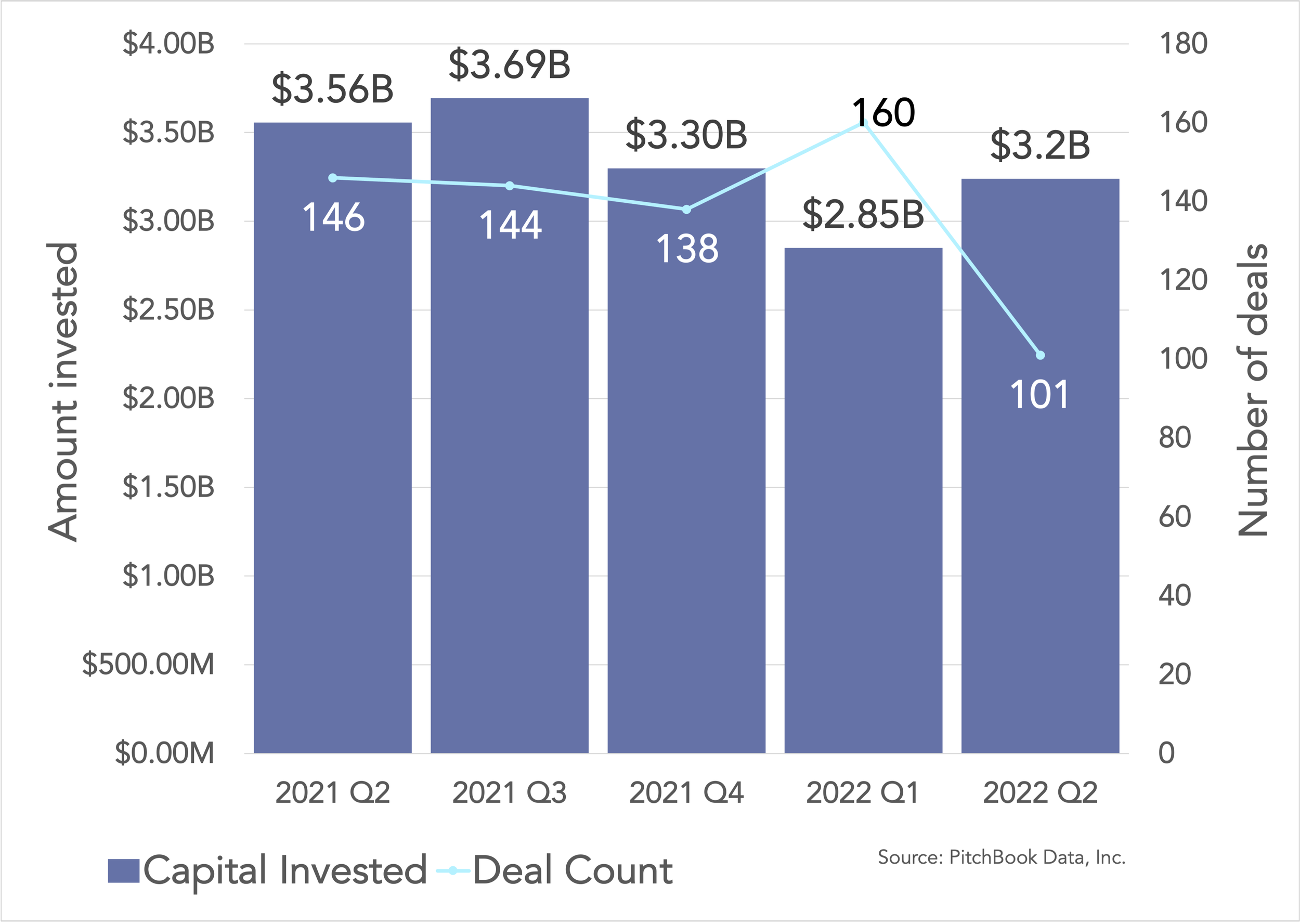

Q2 saw a significant decrease in the number of deals completed, but an increase in overall funding compared to Q1. The massive pullback in the tech and biotech public markets starting in Q3/Q4 2021 in addition to the macro environment uncertainty has led to a fear of a full-on recession. While consumer spending continues to be strong, companies have slowed, delayed or stopped their hiring efforts, with a few implementing painful layoffs. This has led venture to significantly slow their investment pace, although the life science industrials sector seems to be holding steady.

Counter to the doom and gloom narrative, VCs and PEs are sitting on a significant amount of capital with many new funds being closed in the last 12 months. Through the first six months, VCs raised $121.5 billion closed across 415 funds, making 2022 already the second-highest year on record for US VC fundraising. Biopharma and life science industrial players are sitting on a record amount of cash from COVID tailwinds.

Bioprocess as a whole is showing strong growth even as COVID revenue streams fade. The bioprocess divisions are showing 26-33% growth for companies like Danaher, Merck, and Sartorius - driving overall company growth. Investments are still being made to expand bioprocess capacity in cell and gene therapy and CDMOs like Lonza, FujiFilm and others continue to invest. Conferences are coming back en-force with great showings at Built with Biology, BIO, and ESACT.

There is a sense that VCs and acquires are holding out to see what kind of valuations they can capture and what the macro environment will do before getting back into the market.

Venture & Growth Investing in Life Science Industrials

Venture deal making has remained the same and the total amount raised remained elevated. There is a sense that VCs and acquires are holding out to see what kind of valuations they can capture and what the macro environment will do before making significant investments.

Late-stage deals accounted for most of the total deal value. These later-stage investments reflect a continued focus towards revenue generating companies with proof of concept and market fit.

Recommended Reads

Business

Digital twin startup Unlearn raises $50m to advance AI-powered clinical trials

Regenerative medicine gets $22.7B in investments during 2021

SPAC company EureKING looking to raise $158M to form EU based CDMO

MilliporeSigma and Agilent partner on Process Analytical Technologies (PAT)

Manufacturing

Akron Bio aims to ease regen med bottlenecks with new plasmid RNA plant

ThermoFisher to meet single-use demand with $44M plant in Utah

Fujifilm to invest $1.6bn to quadruple CDMO’s mammalian capacity

Research and Development

Multiply labs, ThermoFisher and Charles River partner to develop robotic cell and gene therapy manufacturing

Industrial designer Invetech launches cell and gene therapy manufacturing platform

*Note: reported transaction amounts and timing are subject to change dependent on final closings.